While the world urgently hopes to reduce GHG emissions from fossil fuels and deforestation, the Brazilian Amazon offshore potentially becomes a new frontier for oil companies. The expected impact of oil royalties on the regional GDP is a political driving force pro-exploration. We advocate that the Brazilian Amazon offshore must remain oil exploration-free and that the country could give up its sovereign right to explore oil locally while replacing oil royalties with "green royalties". Therefore, we propose that the region could benefit from creating a trust fund covering the same amount of royalties that the area would receive from the country's decision not to allow oil exploration in the region.

Brazil is uniquely positioned to perform a leading role in the global transition to a sustainable bioeconomy, despite the increasing hardships for collaboration with this purpose at both national and regional levels due to the currently fragmented geopolitical environment (Yang et al., 2024). For instance, the G20 (Group of 19 countries, the European Union, and the African Union) meeting held in Rio de Janeiro (2024) agreed upon High-level Principles on the Bioeconomy.1 This is particularly relevant given that the G20 responds to 75% of the planet’s greenhouse (GHG) gas emissions (Wei et al., 2025). Moreover, the 30th Conference of the Parties (COP30) of the United Nations Framework Convention on Climate Change (UNFCCC) will be hosted by the Amazonian city of Belém, northern Brazil.

However, the country is immersed in major contradictions (Pereira and Viola, 2024). For instance, in COP28 (held in Dubai 2023), Brazil joined the Organization of the Petroleum Exporting Countries+ (OPEC+) shortly after the federal government announced an ambitious "Ecological Transformation Plan" (Brazil, 2023; Política por Inteiro, 2024). These mixed signals suggest political indecision, which is of particular concern given Brazil's unique combination of large significant GHG emissions (Pereira and Viola, 2024) and lush natural wealth (Scarano et al., 2024). Meanwhile, globally, countries are pressed to present new nationally determined contributions (NDC) by February 2025 (Wei et al., 2025), while Brazil has already done so ambitiously at COP29, Baku (Jiang et al., 2025). Of course, replacing oil and gas with renewable energy will take time and demand several aggressive strategies (Holechek et al., 2022) to slash down emissions before 2030 (IRENA and GRA, 2023). For instance, the IPCC (2023) recommended to reduce CO2 emissions by 45% in relation to 2010 levels by 2030 and reaching net zero by 2050 to contain the global temperature increase to 1.5 °C. However, reducing or ending greenhouse gas (GHG) emissions from fossil fuels to pave the path to 1.5/2.0 °C by 2050 now seems increasingly unlikely. The World Meteorological Organization (WMO, 2024) informed that the global mean surface air temperature from January to September 2024 was already 1.54 °C above the pre-industrial average. Furthermore, the United States have withdrawn from the Paris Agreement in the first few days of the new Trump administration in January 2025 (Frumkin et al., 2025) . Meanwhile, although so far global diplomacy largely aimed to converge on compensation targets, it remains hesitant when setting reduction goals for fossil fuel exploration. The climate deal in Dubai 2023 did not call for a "phasing out" of fossil fuels and instead used softer language referring to "transitioning away" and to net-zero emissions (Nevitt, 2023), and the same logic was kept in Baku 2024. However, some progress in climate finance commitments occurred (Jiang et al., 2025). In parallel, at the national and sub-national levels, oil-producing countries such as Brazil see increasing political and economic pressures for oil royalties that seem to keep the search for new oil reserves active (Leão et al., 2024), slowing down the reduction in fossil fuel consumption necessary for the energy transition. Furthermore, no consistent evidence demonstrates that oil royalties can bring economic prosperity and well-being to the local population (Ribeiro et al., 2010; de Seabra et al., 2015) or nature conservation (Rezende et al., 2018).

Brazilian Amazon and the local contextThe Brazilian Amazon is the cradle of planetary biodiversity, unique cultural diversity, and the most critical open-sky carbon stock, equivalent to 10 yr of global emission (Nobre et al., 2021; Carrero et al., 2022; Pezzuti et al., 2024). In parallel, the region is under a dramatic pressure to expand hydrocarbon prospection and exploration, with potential consent by the Brazilian government. Forty-years ago, still in the 1980's, such activities started leading to the onset of the Urucu Clusters: five active oil and gas production onshore fields. This is the largest Brazilian onshore operation, located some 200 km from Manaus (the capital of Amazonas state), now producing 11,000 barrels daily, in marked decline as compared to ten years ago (Fonseca and Marques, 2025). Despite some optimism with the potential of economic and environmental benefits of shifting energy generation from diesel-based to gas-based in isolated areas of the State (Barbosa et al., 2023), the impact of these operations alone and the existing and projected associated infrastructure (e.g., pipeline network of >700 km, railways, waterways, etc.) might negatively impact 164 indigenous lands and areas where 58 isolated people live (Santos e Silva, 2023).

The advance of oil and gas exploration is already happening in neighboring Amazonian countries, often with reportedly negative socioenvironmental impacts (Finer et al., 2013). In Brazil, the contribution of oil royalties to sub-national and national gross domestic product is the main political driving force in favor of exploration in the region, alongside with the expected profit margins for the Brazilian Oil Company, Petrobras. Due to the logic of royalties distribution in Brazil, at sub-national level, this is particularly true for Pará and Amapá States, both holders of large offshore oil and gas reserves. However, like other oil-producing countries, Brazil has no evidence that oil royalty funds can increase social and environmental indicators in poor municipalities. On the contrary, oil royalties are usually associated with growing crime, greenhouse gas emissions, social inequalities, and deforestation, mainly due to local and regional governments poor management of royalties' funds (Filgueira et al., 2020). This is all the more reason for concern in face of the well-known role of the Amazon in climate regulation, and conservation of biocultural diversity (e.g., Almada et al., 2024; Scarano et al., 2024).

The source of political motivation for new oil royalties is based on the Amazon Fan sedimentary basin. This basin has been specially targeted for its deep-water petroleum potential, with structural and stratigraphic traps indicating possible reserves (Manley et al., 1997) in laterally extensive mud-rich sand deposits that are tens to hundreds of meters thick and exceed 100 km in length. This demonstrates a complex depositional environment and highlights the critical need to carefully manage these potentially sensitive Amazonian coastal ecosystems, geological processes, and marine biodiversity. The disruption of seabed habitats, potential for oil spills, and disturbances to sedimentary processes pose significant risks to marine life and the overall health of the oceanic environment (Maslin et al., 2005).

We argue that Brazil has a timely opportunity to give up its sovereign right to explore offshore oil in the Amazon and replace the payment of related oil royalties to the federation, states, and municipalities with what we call "green royalties." Differently from proposals that link Amazon Forest conservation to just keeping the oil underground in the region, we propose that the Brazilian Amazon could benefit from creating a trust fund covering the same amount of royalties that the area would receive from the country’s decision not to allow offshore oil exploration. In this case, the states of Pará and Amapá would benefit the most from green royalties.

In this paper, we start from the premise that Brazil's federal government and Petrobras are willing to start offshore oil exploration in the Amazon and only face resistance from its Ministry of Environment (Rodrigues, 2023). We argue against this exploration based on the following analysis: we 1) estimated the core capital for such a trust fund and speculate on its potential sources; 2) examined the impact of existing oil royalty distribution on socioecological indicators elsewhere in the country; and 3) defined a curve for our proposed green fund based on the estimated offshore oil production curve. Finally, we discuss aspects related to the operation of the fund, the potential relevance to the reputation, and the implications of pioneering the move from discourse to practice related to energy transition to both the Brazilian Oil Company (Petrobras) and the country as a whole in the global scenario.

Material and methodsNecessary investment to establish the Green Royalty FundWe considered the estimated recoverable offshore oil reserves, average oil price, and the life production in the Northern Brazilian Equatorial Margin to calculate the investment amount required to establish a fund capable of compensating Brazilian Amazon states and municipalities for Brazil choosing not to exploit oil in the region. Recent estimates suggest a local significant petroleum potential of up to 10 billion barrels (bi bbl) of recoverable oil reserves.2 This estimate is aligned with the reserves found in the Búzios field within the Santos Basin pre-salt layer in southeast Brazil. To calculate the potential royalties, we applied the historical average royalty rate of 15% to the projected revenues.

The impacts of oil royalties on socioecological indicators: Rio de Janeiro as proxyTo examine the effects of royalty payments on social and environmental indicators, we analyzed the primary beneficiary municipalities in Rio de Janeiro state, southeast Brazil, and their socioecological indicators as proxies for the Amazonian case. Rio de Janeiro state accounts for 80% of all offshore oil reserves in Brazil, with municipalities highly reliant on oil revenues. To identify the primary beneficiary municipalities, we consulted the National Petroleum Agency (ANP) website3 for information on oil and gas revenues received by 92 municipalities in Rio de Janeiro state between 2014 and 2023. For the ten primary beneficiary municipalities of royalty payments and Rio de Janeiro state, we also gathered data on municipal human development and vegetation cover from different years. We obtained the vegetation coverage in each municipality and the state from the MapBiomas platform4 for 2009 and 2022. We consulted the Human Development Index (HDI) for the state of Rio de Janeiro on the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística, IBGE) website5 for the years 2010 and the latest available year, 2021. For the municipalities, we used the index developed by the Federation of Industries of the State of Rio de Janeiro (Federação das Indústrias do Estado do Rio de Janeiro, Firjan), specifically the Firjan Human Development Index6, for the years 2009 and the latest available year, 2016.

Defining the fund's curve based on the estimated oil production curveThroughout history, Campos Basin has already produced 14.3 billion bbl (barrel of crude oil) and Santos Basin 5.6 bi bbl.7 As we have mentioned previously, the estimate is that the Amazonian Equatorial Margin will produce an amount between these two, something close to 10 bi bbl. The estimated curve for the Equatorial Margin was obtained by using the historical average up to year 34 and apportioning the missing amount so that the 10 billion (bbl) could be completed (years 35 to 48). We calculated the fund's curve using the average of the production curve since the amount of royalties follows the amount of product (oil). We estimated the behavior of the royalties' curves and the sizes of the fund to cover the payment of USD 60 billion over 27 years (i.e., to cover the annual royalty payments of 2.2 billion USD to states and municipalities). We designed three scenarios, based on a Normal Distribution Curve: 1) Left skewed, 2) Right skewed, and 3) Constant.

ResultsNecessary investment to establish the Green Royalty FundAssuming an average oil price of USD 67.00 per barrel (the average price estimated from 2030 to 2050 varies between USD 34.00 and USD 84.00, depending on the scenario; IEA, 2023), indicates that the potential of up to 10 billion barrels of recoverable oil reserves could generate USD 670 billion over the 27-year lifespan of their production contracts.8 This projection suggests an average annual revenue of USD 24.8 billion. By applying the historical average royalty rate of 15% to the projected revenues, we estimated an average annual royalty payment of USD 3.7 billion, with USD 1.5 billion allocated to the federal government (40%) and USD 2.2 billion to the states and municipalities (60%), as stated by the regulation9 (Table 1).

Estimates of recoverable oil volume, gross oil revenue, and annual average revenue for 27 years of production in the Northern Brazilian Equatorial Margin. Below are the estimated yearly royalty revenues for the federal government, states, and municipalities and the respective fund size necessary to cover the royalty payments.

| Variable | Estimates |

|---|---|

| Recoverable oil amount | 10 bi barrels |

| Oil gross revenue | USD 670.00 |

| Production life | 27 years |

| Annual average revenue | USD 24.8 billion |

| Total | Federal Government | States and municipalities | |

|---|---|---|---|

| Share of royalties for states and municipalities | 100% | 40% | 60% |

| Annual average Royalty revenue | USD 3.7 billion | USD 1.5 billion | USD 2.2 billion |

| Fund size* | USD 33.1 billion | USD 13.2 billion | USD 19.9 billion |

Finally, to establish a Green Royalties Fund capable of compensating states and municipalities for opting not to engage in oil exploitation, we propose a fund backed by a fixed interest rate equivalent to the current Selic rate (the benchmark for most of the interest rates in the Brazilian financial system) of 11.25%.10 An initial investment of USD 19.9 billion would be necessary to cover the annual royalty payments to states and municipalities. However, if the federal government also participates in the Fund's benefits, the total required investment increases to USD 33.1 billion (Table 1).

The impacts of oil royalties on socioecological indicators: Rio de Janeiro as proxyIn the period between 2014 and 2023, the 92 municipalities in Rio de Janeiro state received nearly USD 10 billion in royalty revenues, with ten of them receiving 63% of this total (Fig. 1). Four municipalities, Maricá, Macaé, Niterói, and Campos dos Goytacazes, received more than USD 4 billion altogether (Fig. 1, Table 2). In this same period, there has been a slight increase in vegetation cover in the state of Rio (1.2%), but with the exception of Macaé (1.5%) and Rio das Ostras (2.4%), in most municipalities the increase was smaller (<0.9%) than the overall state increase. Human development, in turn, declined in most municipalities, whereas overall, the state exhibited a slight increase. We also observed that all municipalities, except Niterói and Rio de Janeiro city, showed lower indices than the state (Table 2).

Socioenvironmental indicators of vegetation cover (2009 and 2022) and human development for the ten primary beneficiary municipalities (2009 and 2016) of royalty payments and the state of Rio de Janeiro (2010 and 2016). Royalty payments data cover the years from 2014 to 2023.

| Vegetation cover (%) | Human Development | Royalty revenue 2014/23 (Million US$) | |||

|---|---|---|---|---|---|

| 2009 | 2022 | 2009/10* | 2016 | ||

| Angra dos Reis | 87.6 | 87.2 | 0.787 | 0.705 | 221.1 |

| Cabo Frio | 7.9 | 7.5 | 0.742 | 0.695 | 326.8 |

| Campos dos Goytacazes | 10.2 | 11.1 | 0.694 | 0.721 | 842.8 |

| Macaé | 33.8 | 35.3 | 0.827 | 0.754 | 1,162.5 |

| Maricá | 34.3 | 35.1 | 0.670 | 0.677 | 1,305.2 |

| Niterói | 35.7 | 35.9 | 0.780 | 0.778 | 859.1 |

| Rio das Ostras | 18.0 | 20.4 | 0.792 | 0.714 | 264.7 |

| Rio de Janeiro | 25.0 | 25.2 | 0.799 | 0.789 | 304.7 |

| São João da Barra | 2.7 | 2.9 | 0.733 | 0.709 | 242.1 |

| Saquarema | 25.3 | 24.8 | 0.719 | 0.673 | 536.8 |

| RJ state** | 28.5 | 29.7 | 0.761 | 0.789 | 9,644.7 |

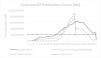

Fig. 2 shows the historical behavior of the main Brazilian oil basins and how the fund would behave in respect to that. We propose a constant fund curve, which would allow for a budget projection for states and municipalities in the long-term. A fund in the order of 19.9 bi USD would fulfill the function of an environmental protection mechanism and simultaneously act as a revenue stabilizer.

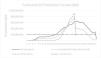

The three curves in Fig. 3 simulate the three possible scenarios for the composition of the Green Fund. The first is a stabilization scenario, in which the value of interest (which replaces royalties) remains constant and demands the least resource mobilization. The second is a scenario in which most of the interest is paid in the initial years, which requires more resources that will be released gradually. The third scenario requires a smaller volume of resources at the beginning but with an increasing demand to achieve the maximum value at the end of the period.

Discussion

Several studies about oil and gas royalty distribution in Brazil confirm our results that, so far, this policy has been largely ineffective in fostering municipal development (Postali and Nishijima, 2011; Tavares et al., 2021). Some marginally positive results have been found by Nishijima et al. (2020) for human capital indicators. For the state of Rio de Janeiro, results are overall so negative that Tavares et al. (2021) speak of a "natural resource curse" (p.381) for local municipalities. This expression – related to the inverse relationship between royalty revenue and socioeconomic development – is broadly used for similar issues in developing countries, such as Ghana (Suleman et al., 2023), Malaysia (Mohamad et al., 2024), Nigeria (Ebimobowei, 2022), whereas some positive cases are found in Colombia depending on the efficiency of municipal management (Collazos-Ortiz and Schakel, 2024).

Based on the recent history and criteria for oil royalty distribution among the federal and State governments, municipalities, and other actors, we estimated that the trust fund for an equivalent green royalty distribution would need a core capital of US$ 19 billion. This amount is feasible since it is comparable to existing trust funds such as FONAFIFO (https://www.fonafifo.go.cr) and Alaska Permanent Fund (APF - https://apfc.org/). The seed capital for the trust fund would come from the National Treasury as a signal of Brazil's commitment to the mechanism. Complementary resources may come from other sources, including international cooperation and voluntary donors. There are three aspects concerning the fund that we believe are worth highlighting. The first one is the "Operation." Given Brazil's already described history of inefficient use of oil royalties, the green royalties would require clear and transparent rules to ensure more efficient resource use, including disbursements in response to socioecological targets achieved by the recipients of the funds. Based on transparent and efficient governance, the Green Royalty Fund may be a powerful tool to protect and restore forests, mangroves, fisheries, rhodolith beds – and all their associated blue and green carbon, and potential for food and medicine production (Aragón and Clüsener-Godt, 2024; Curbelo-Fernandez et al., 2024; Mikkola, 2024; Valli et al., 2018; Valli and Bolzani, 2019) generating additional benefits to the global climate and the Amazon biome. For instance, it has already been shown that the minimal costs to protect 80% of the Amazon ranges from USD 1.7–2.8 billion annually (Silva et al., 2022), which is around 10% of the total estimated fund.

The second aspect is related to "Reputation". Although in our design the green royalties would mean fewer funds transferred to the federation, we trust the significant international credential would compensate for Brazil, which could involve another avenue of potential gains. Internally, such a measure would also have a positive externality: reducing internal political pressures to expand oil exploration as a revenue source for states and municipalities. Furthermore, the Green Royalty Fund approach represents a sustainable source of capital characterized by its longevity and stability over time, distinct from that related to natural resource-based growth - peaking before depletion.

Finally, the third element is the "Transition" from a fossil-fuel economy to a sustainable and fair bioeconomy. We estimated that half of the potential costs of implementing the oil extraction operation (US$ 175 billion)11 could be invested in other strategies announced by Petrobras, such as their Venture Capital Fund, Carbon Capture, Utilization, and Storage (CCUS), biofuels, renewable energy, and Nature-Based Solutions (NBS). If so, they could significantly advance the sector's transition towards a more sustainable energy landscape and also move initiatives, like the announced Plan for Ecological Transformation (Brazil, 2023), from discourse to practice.

The example of the other Brazilian tropical rainforest is very significant. Governance and protection have increased overtime in the Atlantic rainforest but in a reactive fashion, after impacts and loss have occurred (Pinto et al., 2023). The Amazon and the planet cannot afford further mistakes and delays. The planet faces a critical challenge: the more we rely on oil burning, the more we contribute to deforestation and degradation in the Amazon, leading to increased greenhouse gas emissions. To safeguard Amazon and its crucial global environmental services for future generations, avoiding new hydrocarbon exploration and keeping what remains of the region free of oil is imperative. The Amazon is one of the last remaining extensive forests on Earth, pivotal in preserving global biodiversity and combating climate crises (Reid and Lovejoy, 2022). Our proposal for the green fund to pay royalties offers a pathway to sustainable development in the Brazilian Amazon while protecting the forest and its environmental services.

The authors declare that they have no known conflict of interest.

ACFA and FRS thank the Unesco Chair on Planetary Wellbeing and Anticipatory Regeneration at the Museum of Tomorrow and its partner institutions.

https://wcbef.com/wp-content/uploads/2024/12/2024-09-11-high-level_principles_on_bioeconomy-final_version.pdf.

https://www.cnnbrasil.com.br/economia/macroeconomia/estudo-da-petrobras-indica-que-bloco-na-foz-do-amazonas-possa-conter-56-b-barris-de-petroleo-diz-ministro/#:%E2%88%BC:text=Potencial%20de%20explora%C3%A7%C3%A3o&text=Nele%2C%20est%C3%A1%20descrito%20que%20a,menos%206%20bilh%C3%B5es%20de%20barris.https://www.cnnbrasil.com.br/economia/estudo-da-petrobras-indica-que-bloco-na-foz-do-amazonas-possa-conter-56-b-barris-de-petroleo-diz-ministro/#:%E2%88%BC:text=Potencial%20de%20explora%C3%A7%C3%A3o&text=Nele%2C%20est%C3%A1%20descrito%20que%20a,menos%206%20bilh%C3%B5es%20de%20barris.

https://www.gov.br/anp/pt-br/assuntos/exploracao-e-producao-de-oleo-e-gas/desenvolvimento-e-producao.

https://brasil.mapbiomas.org/.

https://cidades.ibge.gov.br/.

https://www.firjan.com.br/ifdm.

Information provided by the ANP: https://www.gov.br/anp/pt-br/assuntos/exploracao-e-producao-de-oleo-e-gas/desenvolvimento-e-producao.

https://www.gov.br/anp/pt-br/assuntos/exploracao-e-producao-de-oleo-e-gas/desenvolvimento-e-producao.

- Home

- All contents

- Publish your article

- About the journal

- Metrics